Q3 TD Cowen/AFS Freight Index shows fuel prices and supply-side constraints driving up rates across modes, though demand-side recovery still tentative

- Continued capacity reductions, rising fuel prices squeeze truckload pricing to a four-year high

- LTL rates reach another record high driven by spiking fuel prices, while FedEx Freight spinoff and Amazon entry disrupt competitive landscape

- Fuel continues to shape sky-high parcel rates, but FedEx and UPS face growing pressure from Amazon and other alternative carriers

ATLANTA (July 14, 2026) – AFS Logistics and TD Cowen announce the third quarter (Q3) 2026 release of the TD Cowen/AFS Freight Index, a snapshot with predictive pricing for truckload, less-than-truckload (LTL) and parcel transportation markets. This quarter’s index shows the effects of oil price shocks rippling through shipping markets, with Q2 data showing rates actualized at higher-than-projected levels. Forward-looking estimates for Q3 expect rates to hold steady at elevated levels, though renewed conflict in the Middle East and the associated impact on fuel prices could threaten even higher costs.

“With this edition of the freight index, the fuel numbers tell the story. In Q2, diesel prices rose about 51% compared to January and February levels, while jet fuel prices were up 90% compared to Q2 of last year,” says Andy Dyer, CEO, AFS Logistics. “Beyond the direct impact of higher freight bills paid by shippers, these price movements also have second-order effects that squeeze rates higher. Smaller truckload carriers working on tight margins may park trucks and wait for fuel prices to revert to more palatable levels before returning to operation, further restraining capacity amid a supply-side market correction.”

Truckload: Continued supply-side correction drives rates to four-year high

Despite some encouraging signs, a demand-driven recovery is yet to materialize. The American Trucking Association’s (ATA) tonnage index showed the sixth-straight month of year-over-year (YoY) increase in May, but that same month was also the second straight month of decline from the March peak. Macroeconomic signs show a similarly mixed outlook, with moderate gross domestic product growth but limited spending and resurgent inflation. But while demand signals remain tentative, the capacity contraction is fully underway. Heightened regulatory enforcement action has reduced the driver pool by more than 48,000 over the past year and together with continued carrier exits, is resulting in significantly tighter capacity.

That supply-side pressure and spiking fuel costs powered truckload rates to their highest levels in 15 quarters, reaching 16% above the January 2018 baseline in Q2. That capacity crunch-driven momentum is expected to continue in Q3, with the truckload rate per mile index projected to reach 17.7% — a four-year high and 11% YoY increase.

LTL: Exploding fuel surcharges elevate rates to new highs

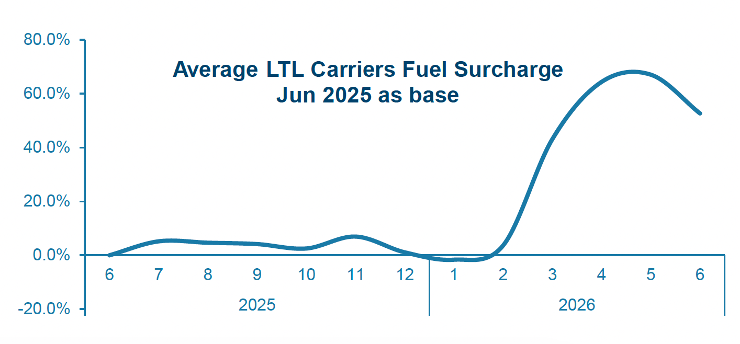

After one quarter of weight per shipment and cost per shipment moving in tandem, the two metrics once again de-coupled in Q2, with falling weight reflecting continued softness in industrial and manufacturing demand alongside ongoing modal shifts. But while longstanding carrier pricing discipline played a role in keeping rates elevated, significantly higher fuel prices pushed costs to new heights. The average LTL fuel surcharge in Q2 2026 surged to over 60% above the June 2025 level, driven by 51% higher diesel prices compared to the early 2026 average.

The Q2 2026 rate per pound index was projected to reach a record high, but reached even greater heights than expected, primarily driven by the prolonged conflicts in the Middle East boosting average fuel cost per pound by 46% quarter-over-quarter (QoQ). Looking ahead to Q3, the LTL rate per pound index is expected to sustain historically elevated levels and reach a new high of 76.8% above the January 2018 baseline, up 0.2% QoQ and 5.9% YoY.

“Q2 showed that carriers’ pricing strategies include the ability to not only secure rate increases and strategically valuable volumes, but capture volatile fuel costs,” says Mich Fabriga, Vice President of LTL Pricing, AFS Logistics. “But aside from fuel, the competitive landscape is experiencing some major shifts. While near-term impact may be limited, Amazon’s full-scale entry into the LTL market signals a major force for the future and the completion of the FedEx Freight spinoff frees a major player to compete without their parcel business tying their hands.”

Parcel: Surcharge fatigue and viable alternatives turn up competitive pressure

Shipper frustration with seemingly constant changes to fuel, peak and other surcharges, together with the emergence of viable alternative carriers, adds up to a new era of competition in the parcel market. Regional and last-mile carriers, such as OnTrac, GLS, Spee-Dee, Veho and UniUni, more than doubled their volumes from 2024 to 2025, according to Pitney Bowes data. But of even greater significance is Amazon Supply Chain Services opening its network to external shippers. While the near-term scale of this market entry may be limited, long-term implications for the pricing power of FedEx and UPS are meaningful, particularly in segments like residential and small-to-medium-sized business where Amazon has particularly strong network density.

“This shifting carrier landscape is a welcome development for shippers who have long sought relief from two dominant players that seemingly moved in lockstep,” says Mingshu Bates, President of Parcel and Chief Analytics Officer, AFS Logistics. “But capitalizing on these savings opportunities requires managing significant complexity, both in terms of navigating a carrier landscape with highly variable service offerings and geographic reach, and the technology infrastructure necessary to rate shop parcels and execute fulfillment.”

In ground parcel, continued changes to fuel surcharge tables by FedEx and UPS ensure that heightened fuel surcharge revenue holds firm even as actual diesel prices eventually fall. For example, if diesel falls to $4.00 per gallon, shippers will still pay a 24-24.5% fuel surcharge, compared to just 21% under last year’s tables. In Q2 2026, spiking diesel prices translated into average net fuel surcharge per package increasing 40% YoY. Discount levels also declined QoQ, with both FedEx and UPS tightening pricing in Q2, a reversal of the Q1 dynamic of FedEx offering deeper discounts and UPS tightening pricing. After reaching a record high of 42.4% above the January 2018 baseline in Q2 2026, the ground parcel rate per package index is projected to remain elevated but ease in line with seasonal trends, falling 2.6% QoQ to 38.7%. This Q3 figure still represents a 5.2% YoY increase, on track to make 2026 the year with the highest cost per package on record.

In Q2, discounting in express parcel took the opposite approach of ground. Not only did discount levels increase, but for large customers, a divergence emerged as FedEx deployed deeper discounts while UPS kept pricing tighter. But elevated fuel surcharges, higher billed weight and more premium services proved a potent formula for elevated rates, with the express parcel rate per package index reaching a new high of 15.5% above the January 2018 baseline in Q2. Looking ahead, the cumulative effect of carrier changes to measurement rounding rules and additional handling surcharge policies will keep average billed weight elevated, and demand surcharges are expected to return toward the end of Q3, adding further upward pressure. The result is another record high, with Q3 expected to reach 15.8% above the January 2018 baseline — up 11.1% YoY.

About the TD Cowen/AFS Freight Index

The TD Cowen/AFS Freight Index launched in October 2021, offering a unique perspective on the transportation market through its dataset, forward-looking view and perspective on parcel shipping. Expected rate levels are derived from billions in annual transportation spend across all modes and includes actual net charges that factor in accessorials such as fuel surcharges. Past performance and machine learning produce predictions for the remainder of the quarter, set against a baseline of 2018 rates for each mode.

About AFS Logistics

AFS is a group of shipping strategists that helps more than 1,800 companies across 35 countries better understand their freight costs. The company has over $11 billion in transportation spend under management, and uses that data along with decades of truckload, LTL and parcel experience to help advise, optimize and manage client shipping programs. AFS provides support throughout the process of buying, planning, executing and settling transportation services, constantly assessing performance to ensure shippers only pay what they should and get the service and operational outcomes they deserve.

The company was founded in 1982 and employs more than 380 teammates across the U.S. and Canada. AFS is regularly part of the Inc. 5000 list of fastest growing companies. To learn more, visit www.afs.net.

###

Media contact: Dan Gauss Koroberi 336.409.5391 [email protected]